This is a summary of the recent performance of a wide range of excellent Tactical Asset Allocation (TAA) strategies, net of transaction costs. These strategies are sourced from books, academic papers, and other publications. While we don’t (yet) include every published TAA model, these strategies are broadly representative of the TAA space. Learn more about what we do or let AllocateSmartly help you follow these strategies in near real-time.

Commentary:

Tactical Asset Allocation generally underperformed the benchmark in November.

Tactical Asset Allocation generally underperformed the benchmark in November.

TAA entered the month positioned somewhat defensively (see data dump below), but US equities went on to turn in a strong performance for the month (ex. SPY +3.6%, IWM +4.1%), leading most strategies to lag the US-centric 60/40. TAA has returned to a more aggressive allocation for December.

TAA trails YTD:

This has been the year of the headfake for TAA. While TAA did a good job controlling market losses during the pullbacks in late-2018 and twice this year, in all cases those losses proved to be short-lived. TAA was positioned too defensively for the subsequent market rebound, and as a result, trails YTD.

To some degree, this is the price of doing business for trend-following/momentum types of strategies. At some point, TAA’s cautious nature is going to save the portfolio from significant loss (ex. 2000-02 and 2007-08), but in the meantime, that risk adversity makes TAA prone to getting stuck on the sidelines when those losses don’t develop.

Data dump:

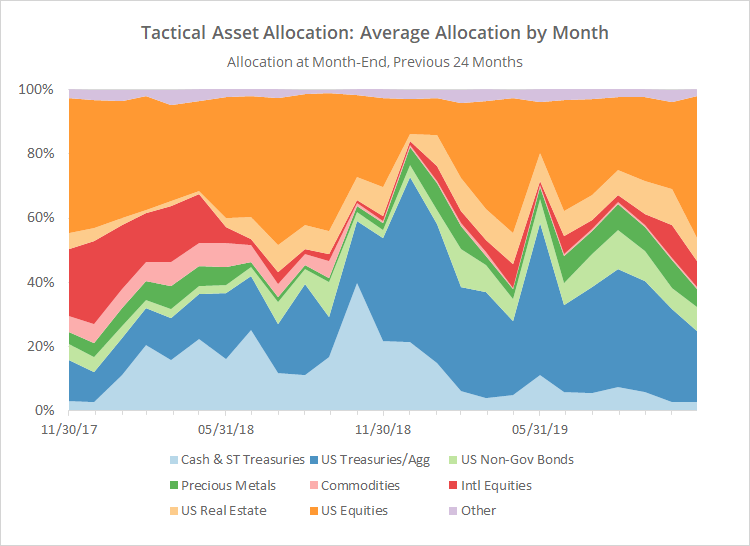

With such a large pool of published strategies to draw on (54 and counting), we’re able to draw some broad conclusions about the state of TAA. The following two charts help to show trends in the asset classes that TAA as a whole is allocating to over time.

The first chart shows the average month-end allocation to categories of assets by all of the strategies that we track. For example, “US Equities” may include everything from the S&P 500 to individual stock market sectors. Defensive assets tend to be at the bottom of the chart, and offensive at the top. The data on the far right of the chart reflects where TAA stood as of the end of the most recent month.

The most significant shift in allocation at month-end was out of mostly defensive assets and into US equities (+17%).

In the second chart below, we’ve combined average TAA allocation into even broader categories: “risk on” (equities, real estate and high yield bonds) versus “risk off” (everything else). We realize that some asset classes don’t fit neatly into these buckets, but it makes for a useful high level view.

{kind=link}

{kind=link}

We invite you to become a member for about a $1 a day, or take our platform for a test drive with a free limited membership. Put the industry’s best tactical asset allocation strategies to the test, combine them into your own custom portfolio, and then track them in near real-time. Have questions? Learn more about what we do, check out our FAQs or contact us.