This is a summary of the January performance of a number of excellent tactical asset allocation strategies. These strategies are sourced from books, academic papers, and other publications. While we don’t (yet) include every published TAA model, these strategies are broadly representative of the TAA space. Read more about our backtests or let AllocateSmartly help you follow these strategies in near real-time.

Commentary:

Tactical asset allocation turned in a strong performance in January, with positive results (almost) across the board. It was hard to go horribly wrong, with most significant asset classes also up for the month. Notable winning asset classes included gold (GLD +5.4%) and just about anything related to international equities (ex. emerging and developed market equities, EEM +6.7% and EFA +3.3%).

Tactical asset allocation turned in a strong performance in January, with positive results (almost) across the board. It was hard to go horribly wrong, with most significant asset classes also up for the month. Notable winning asset classes included gold (GLD +5.4%) and just about anything related to international equities (ex. emerging and developed market equities, EEM +6.7% and EFA +3.3%).

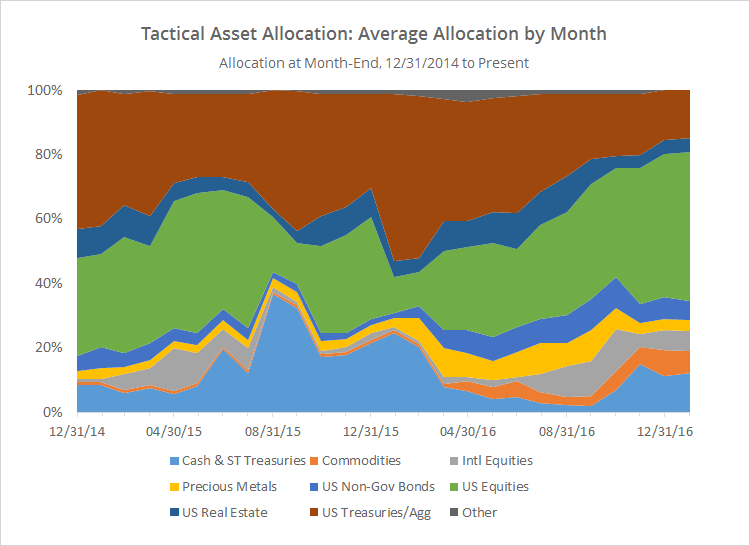

Overall, the strategies that we track continue to increase exposure to risk assets. To illustrate, the chart below shows the average allocation to broad categories of assets by the 31 strategies that we track, as of the end of each month since EO’2014.

Note that allocation to US equities (green) is now at a sample high of 47%, meaning that, on average, the strategies that we track are currently nearly half allocated to some flavor of US equities. Conversely, allocation to US Treasuries is now at a sample low of 15%.

In the next graph we take an even broader view, combining asset classes into just two categories: “risk on” (equities, real estate and high yield bonds) versus “risk off” (everything else). I realize that some asset classes don’t fit neatly into these buckets, but it makes for a useful high level summary.

Risk assets are now at a sample high of 61%. That’s not necessarily a bad thing, but there is significant exposure to investors here if the market stumbles in February.

We invite you to become a member for less than $1 a day to track these 31 tactical asset allocation models in near real-time, or take our platform for a test drive with a free limited membership. Have questions? Learn more about what we do, check out our FAQs or contact us.