(…but that won’t always be the case)

Over the last 15+ years, diversification (as opposed to market timing) has been a huge drag on Tactical Asset Allocation (TAA) performance, to the tune of 2.1% per year compared to the 60/40 benchmark. That “diversification drag” has been mostly due to US stock market dominance over almost all other asset classes over that period. TAA must use market timing to overcome this drag.

Of course, that’s not the whole story: (1) the benefit of diversification ebbs and flows and the next 15 years may be entirely different, and (2) diversification provides other benefits like reducing risk. But over the last 15 years, it’s been an important story.

Note: We track 100+ TAA strategies, so these results are broadly representative of TAA as a trading style.

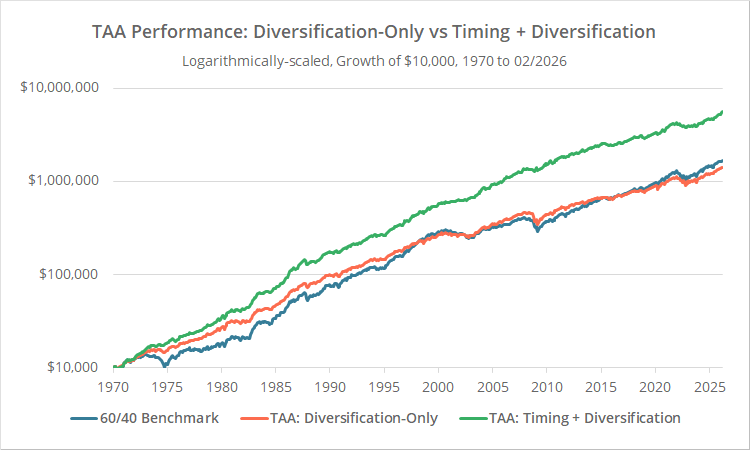

In the graph above we show three equity curves since 1970. Green is the average return of the 100+ TAA strategies we track, and blue is the 60/40 benchmark (60% SPY/40% IEF, rebalanced monthly).

Orange represents a hypothetical portfolio that holds the average allocation of 100+ TAA strategies since inception, up to that point in time, rebalanced monthly. This is like removing the market timing from TAA and treating the average TAA allocation as a buy & hold portfolio.

We can then break down market timing versus diversification as follows:

- Market Timing = Average TAA Strategy / Average TAA Allocation

- Diversification = Average TAA Allocation / Benchmark

- Total Performance = Market Timing + Diversification

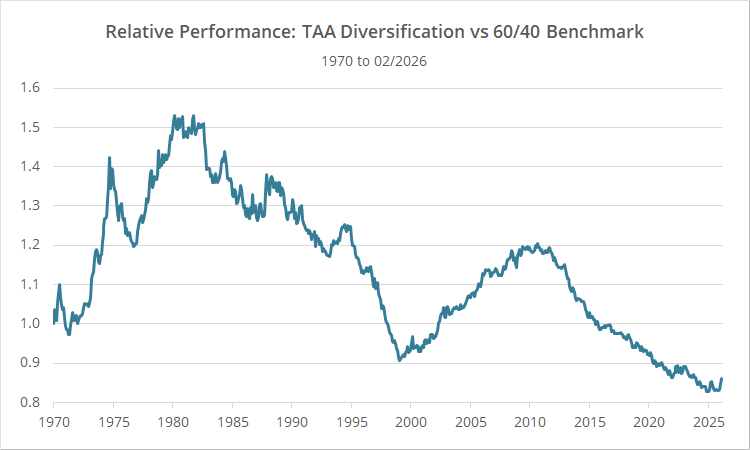

Diversification-only since 1970 looks as follows:

Through the 70’s and aughts, diversification provided a beneficial tailwind for TAA returns, mostly due to outperformance in alternative asset classes like gold and commodities.

Through all other decades, diversification has been a drag on return (but not necessarily risk-adjusted return, more on this later). Since August 2010, that drag has been 2.1% annualized.

TAA can still outperform through market timing (i.e. what TAA is holding at this moment compared to what it tends to hold), but it’s a headwind it must overcome.

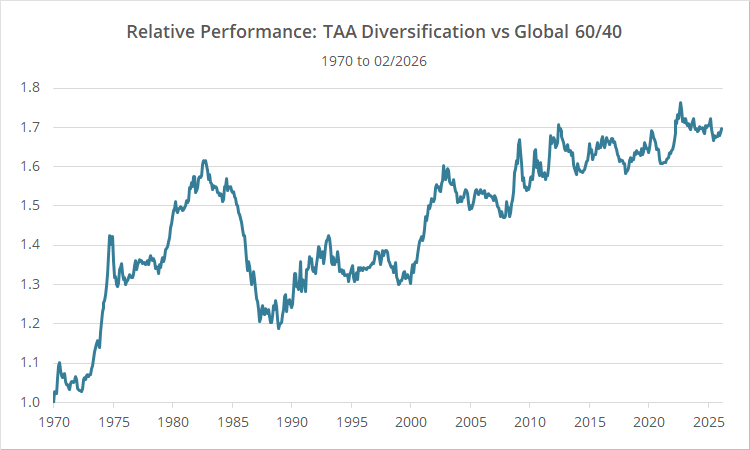

A Global 60/40:

The US 60/40 benchmark is not the only benchmark in town. What if we instead used a global 60/40 benchmark represented by 60% ACWI, 20% IEF, 20% BWX, rebalanced monthly.

For the most part, excluding the 1980’s, TAA’s diversification has been neutral to slightly beneficial compared to the global 60/40. The global 60/40 has consistently been a much easier hurdle to beat due to ex-US underperformance.

If our primary interest was making strategies look good, we would benchmark to the global 60/40. In some ways it’s more relevant. But the US 60/40 is ubiquitous and best understood by investors, so we use it as our default (members: other benchmarks are available in the Compare Tool).

Diversification provides other benefits:

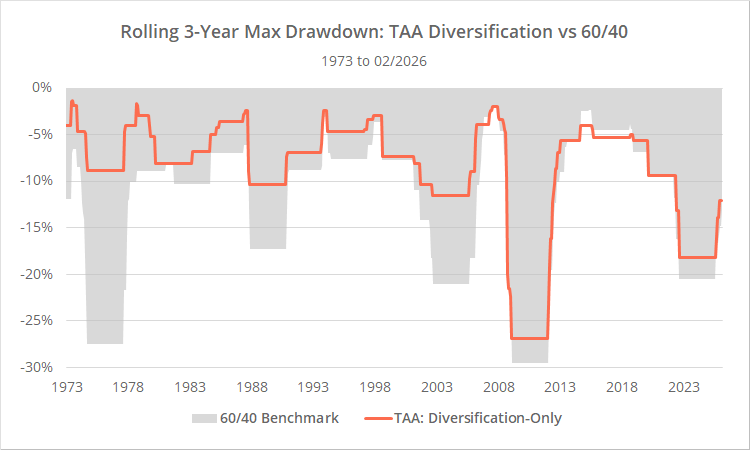

Of course, return isn’t the whole story. Diversification provides other benefits, namely reducing risk (drawdowns, volatility, path risk, etc.) and increasing risk-adjusted returns.

To illustrate, below we show the rolling 3-year max drawdown of the 60/40 benchmark (grey) versus our buy & hold “diversification-only” portfolio (orange) since 1970.

Note how diversification alone significantly pared down all major drawdowns except the Global Financial Crisis in 2007/2008 and the 2022 bear market.

Interestingly, TAA would have still done extremely well during the GFC and reasonably well in 2022, but that was all market timing. Diversification didn’t help much in those cases.

Outro:

The takeaway from all of the above is not “diversification is bad”. The opposite is true.

Even though, as tactical investors, we are adjusting our portfolios throughout the year, our actual investment horizon spans multiple decades. And over that long horizon, diversification is likely a net positive to the portfolio.

Having said that, it’s helpful to understand when the present market is increasing friction to our investment approach. Over the last 15+ years, diversification has acted as a headwind that TAA must overcome with market timing. It’s been a friction to the tune of 2.1% annually.

That won’t always be the case. It could be tomorrow or it could be another decade from now, but at some point, diversification will again provide a tailwind to TAA returns. In the meantime, we will stay the course and benefit from the risk reduction that diversification provides.

Lastly, note that all of the above applies to most diversified buy & hold portfolios as well. Popular B&H portfolios will be similar to the “diversification-only” results. Where TAA and B&H differ is in the additional market timing component that TAA provides.

New here?

We invite you to become a member for about a $1 a day, or take our platform for a test drive with a free membership. Put the industry’s best tactical asset allocation strategies to the test, combine them into your own custom portfolio, and follow them in real-time. Learn more about what we do.